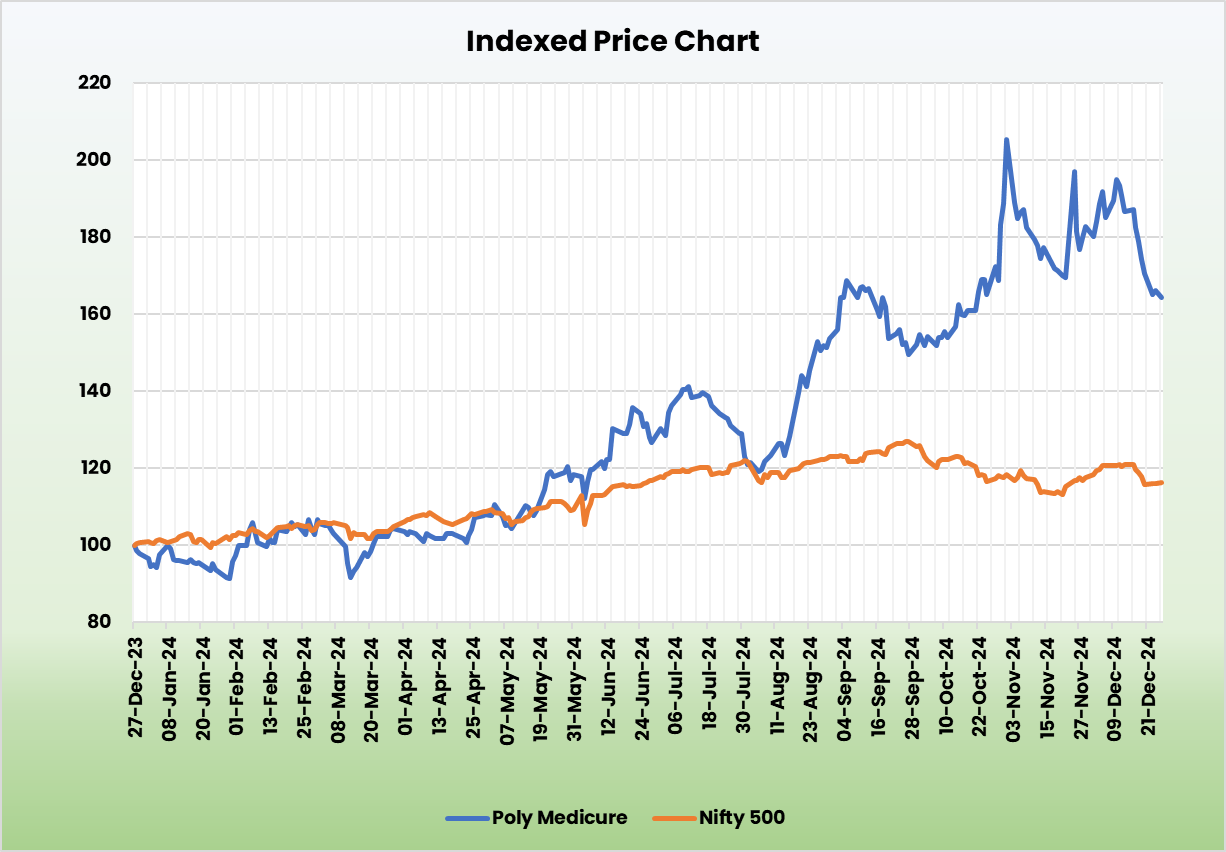

Poly Medicure Ltd – Key participant in medical gadgets area

Poly Medicure Ltd., based in 1995 and based mostly in New Delhi, is a number one producer of medical gadgets throughout infusion remedy, oncology, urology, crucial care, and extra. As India’s prime medical gadget exporter for 12 years, the corporate operates 12 manufacturing amenities and an R&D middle, producing 1.5B gadgets yearly. With over 200 gadgets in its portfolio and purchasers in 125+ nations, Poly Medicure holds 400 patents, with 44 extra pending globally.

Merchandise and Companies

- Oncology, infusion remedy, cardiology, and gastroenterology merchandise

- Urology, anesthesia, and respiratory care options

- Dialysis methods and COVID care merchandise

- Surgical and wound drainage gadgets

- Blood assortment methods and blood administration instruments

- Key merchandise embrace:

- Cannulas and catheters

- Needles and syringes

- Blood baggage and assortment tubes

- Fast diagnostic kits

Subsidiaries: As of FY24, the corporate has 5 subsidiaries and one affiliate firm.

Development Methods

- Renal Sector Enlargement: Investing in reasonably priced renal care with pain-reducing dialysis merchandise, concentrating on income progress from ₹90 crore to ₹140-150 crore by FY25. Plans embrace doubling capability and putting in 500 renal machines.

- Capability Development: Establishing 4 new vegetation with a ₹500 crore funding, boosting manufacturing capability to 1.7-1.8 billion items yearly by FY25.

- Cardiology and Important Care: Increasing market share via import substitution, new merchandise, and a ₹1,000 crore QIP for manufacturing and capability enlargement.

- Gross sales Crew Development: Including 100 salespeople in FY25, specializing in crucial care and cardiology markets.

- Automation and Attain: Enhancing automation and leveraging new vegetation to broaden home and worldwide markets.

Operational Efficiency

Q2FY25

- Income: ₹420 crore, up 25% YoY (Q2FY24: ₹337 crore).

- EBITDA: ₹115 crore, a 37% YoY progress (Q2FY24: ₹84 crore).

- Web Revenue: ₹87 crore, up 40% YoY (Q2FY24: ₹62 crore).

- Margins:

- EBITDA margin improved from 25% to 27%.

- Web revenue margin elevated from 18% to 21%

FY24

- Income: ₹1,376 crore, up 23% YoY, pushed by strong demand and enterprise enlargement.

- EBITDA: ₹419 crore, a 38% progress YoY, reflecting operational efficiencies.

- Web Revenue: ₹258 crore, up 44% YoY, supported by robust margin enhancements.

Monetary Efficiency (FY21-24)

- Sturdy Development: Achieved a income CAGR of 21% and a internet revenue CAGR of 24% over the previous 3 years (FY21-FY24).

- Constant Returns: Maintained a 3-year common ROE of 16% and ROCE of 20%, reflecting environment friendly capital utilization.

- Sturdy Capital Construction: Sturdy monetary stability with a low debt-to-equity ratio of 0.06.

Business outlook

- Authorities Initiatives: Driving competitiveness in biotechnology, medical gadget manufacturing, and healthcare.

- Focus Areas: Manufacturing of disposables (catheters, syringes, feeding tubes) and implants (cardiac stents, intraocular lenses).

- Import Dependency: India depends on imports for 70-80% of medical gadgets, making the sector underdeveloped.

- Make in India Initiative: Prioritized to scale back import dependence and enhance home manufacturing.

- Market Development:

- Diagnostic gear market anticipated to achieve US$ 6 billion by 2027 (up from US$ 4 billion in 2023).

- The Indian medical gadgets market is projected to develop at a CAGR of 16.4%, reaching US$ 5 billion by 2030.

Development Drivers

- Stricter Laws: Enhanced authorities laws and obligatory requirements for importing medical gadgets are anticipated to drive demand for localized merchandise.

- 100% FDI Allowed: 100% international direct funding beneath the automated route is permitted for greenfield prescription drugs and medical gadget manufacturing.

- Union Finances Allocation: Rs. 89,287 crore allotted to the healthcare sector within the Union Finances 2024-25, boosting business progress.

Aggressive Benefit

Poly Medicure Ltd operates in a aggressive panorama with gamers like Tarsons Merchandise Ltd and Centenial Surgical Suture Ltd. Nevertheless, Poly Medicure stands out because it doesn’t have any listed opponents of comparable market capitalization and scale of operations. The corporate is producing superior returns on invested capital, supported by constant income progress, additional solidifying its place available in the market.

Outlook

- Income Development: Achieved 23% income progress in H1FY25, on monitor to satisfy FY25 goal of 22-24%.

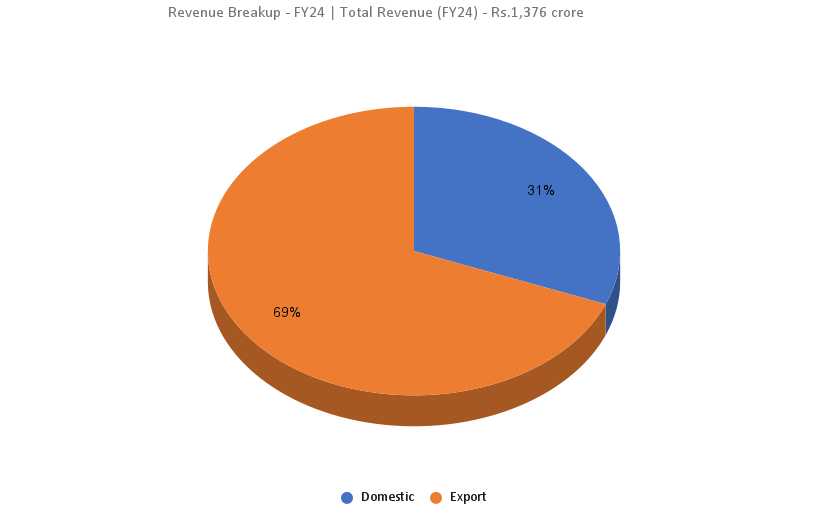

- Income Combine: 70% from exports, 30% from home markets, with plans to keep up this ratio.

- EBITDA Margin: Steering of a 100-150 foundation factors enchancment in FY25.

- Capital Expenditure: Rs. 250 crore allotted for FY25, with Rs. 150 crore already spent in H1FY25, primarily funded by inside accruals.

- Product Launches: Plans to launch 10-12 merchandise yearly, with 20-30 merchandise in growth for the subsequent 2-3 years.

Valuation

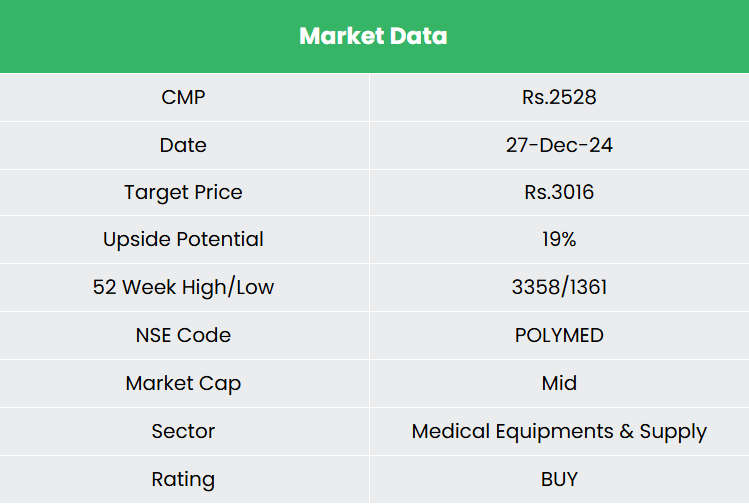

We count on Poly Medicure Ltd to proceed its progress momentum, pushed by its robust presence within the fast-growing medical disposable section, main market share in key classes, entry into bigger markets, enlargement into margin-accretive segments, and robust financials. We advocate a BUY ranking on the inventory with a goal value (TP) of Rs. 3,016, 61x FY26E EPS.

Dangers

- Foreign exchange Danger: With vital operations in international markets, the corporate is uncovered to foreign exchange danger. Unexpected actions within the foreign exchange market might adversely influence its monetary efficiency.

- Aggressive Danger: The medical gadget business is present process a transformative part, with technological developments and new entrants rising competitors, posing dangers to market share and profitability.

Notice: Please be aware that this isn’t a suggestion and is meant just for instructional functions. So, kindly seek the advice of your monetary advisor earlier than investing.

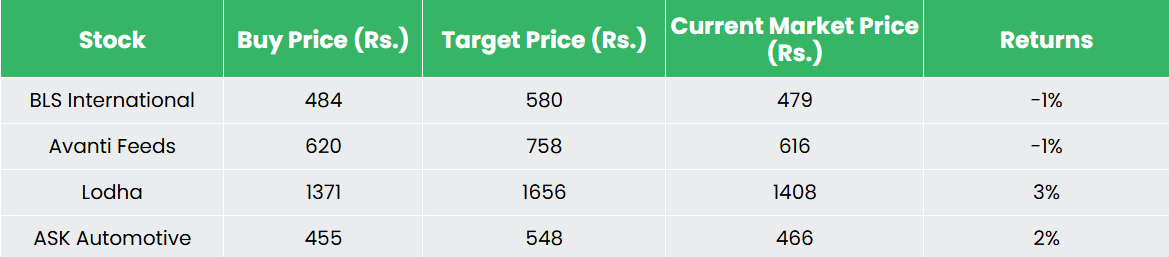

Recap of our earlier suggestions (As on 27 December 2024)

BLS International Services Ltd

Different articles you could like

Publish Views:

120