")

How merely can we make investments with out getting too easy? Three of my largest holdings are multi-cap core funds held in accounts managed by Constancy, Vanguard, or myself. I personal Vanguard Whole Inventory Market Index ETF (VTI), Constancy Strategic Advisers US Whole Inventory (FCTDX), and Vanguard Tax-Managed Capital Appreciation Admiral (VTCLX). What’s beneath the hood of those funds and the way nicely do they carry out in comparison with the market?

In line with the Refinitiv Lipper U.S. Mutual Fund Classifications, multi-cap core funds “by portfolio follow, put money into quite a lot of market capitalization ranges with out concentrating 75% of their fairness belongings in anyone market capitalization vary over an prolonged time period. Multi-cap core funds sometimes have common traits in comparison with the S&P SuperComposite 1500 Index.”

We’re going to see on this article that the efficiency of those multi-cap funds varies extensively. This text is split into the next sections:

UNDERSTANDING MULTI-CAP FUNDS

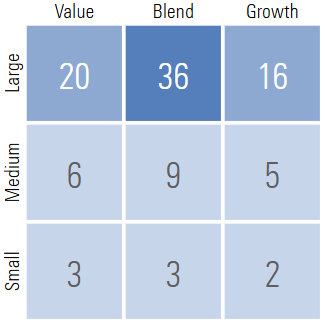

Let’s begin with the Vanguard Whole Inventory Market ETF (VTI) for example. VTI outperformed 80% of the multi-cap core funds on this examine. It holds 3,653 shares with 30% of its belongings within the prime ten holdings. The inventory model weight based on Morningstar is proven in Desk #1.

Desk #1: VTI Inventory Type Weight

Supply: Morningstar

Morningstar provides VTI three stars and a Gold Analyst Ranking. In line with Morningstar:

“Vanguard Whole Inventory Market funds supply highly-efficient, well-diversified and correct publicity to the whole U.S. inventory market, whereas charging rock-bottom charges—a recipe for fulfillment over the long term.

The funds monitor the CRSP US Whole Market Index, which represents roughly 100% of the investable U.S. alternative set. The index weights constituents by market cap after making use of liquidity and investability screens to make sure the index is simpler to trace.”

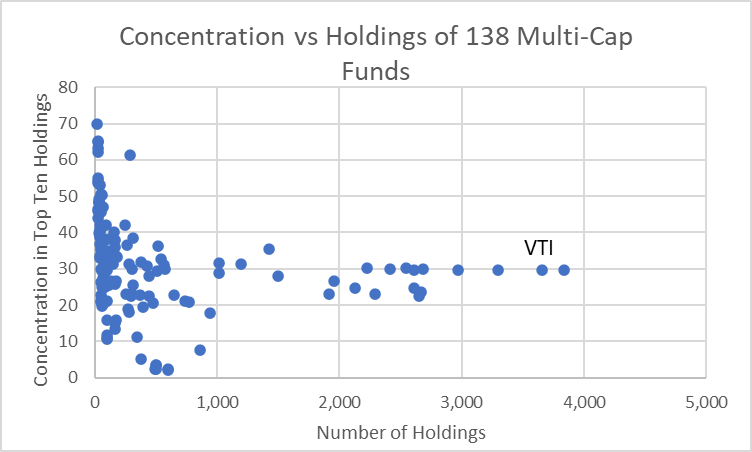

I chosen a big pattern (138) of Multi-Cap funds excluding those who use a “fund of funds technique”. The focus within the prime ten holdings is proven versus the variety of holdings in Determine #1. There are solely a pair dozen funds that observe a real complete market method.

Determine #1: Multi-Cap Core Fund Focus Versus Variety of Holdings

Supply: Creator Utilizing MFO Premium fund screener and Lipper world dataset.

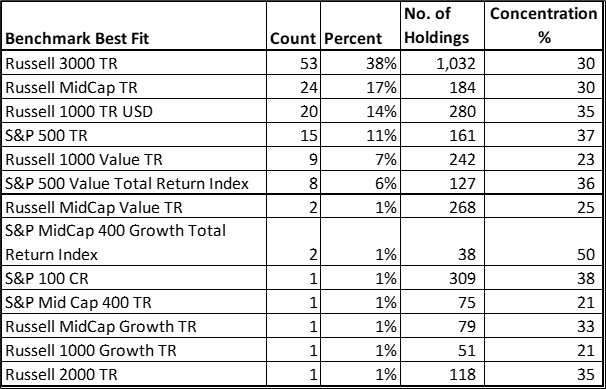

I used the Mutual Fund Observer Multi-Search Software to summarize the “Benchmark Finest Match” in Desk #2. The benchmark, variety of holdings, and focus will clarify plenty of the efficiency variance. As well as, the median focus within the US is 95%, whereas about 15% of the multi-cap core funds have greater than 15% invested exterior of the US.

Desk #2: Multi-Cap Core Fund Finest Match Benchmark, Focus, Holdings

Supply: Creator Utilizing MFO Premium fund screener and Lipper world dataset.

UNIVERSE OF MULTI-CAP CORE FUNDS

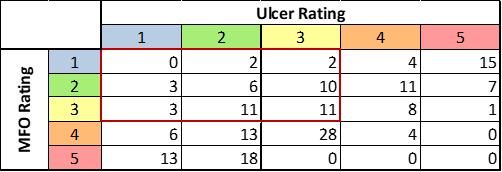

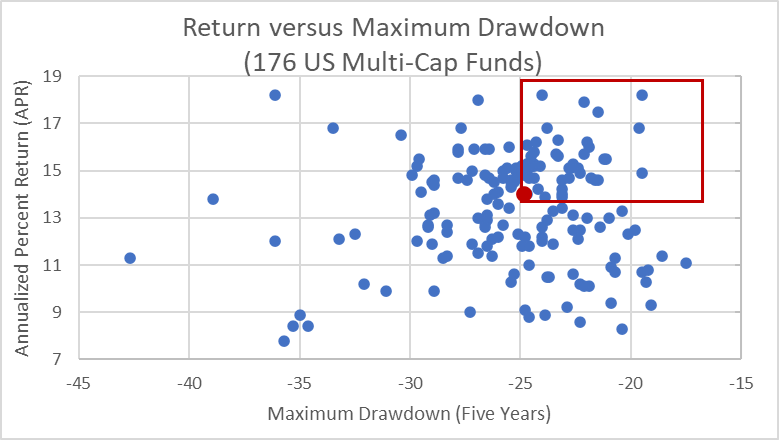

There are 222 multi-cap mutual funds and trade traded funds which might be 5 years outdated or older. I chosen 176 (79%) US Fairness Multi-Cap No-load Mutual Funds and Alternate Traded Funds which might be open to new buyers, and have not less than fifty million {dollars} in belongings beneath administration. Desk #3 exhibits the funds by Ulcer Ranking (a measure of depth and period of drawdown) and MFO Ranking (risk-adjusted return) based mostly on quintiles. The pink rectangle represents the 48 (27%) funds which have each common or larger risk-adjusted returns and common or decrease threat (Ulcer Index).

Desk #3: Multi-Cap Core Funds MFO Ranking versus Ulcer Ranking (5 Years)

Supply: Creator Utilizing MFO Premium fund screener and Lipper world dataset.

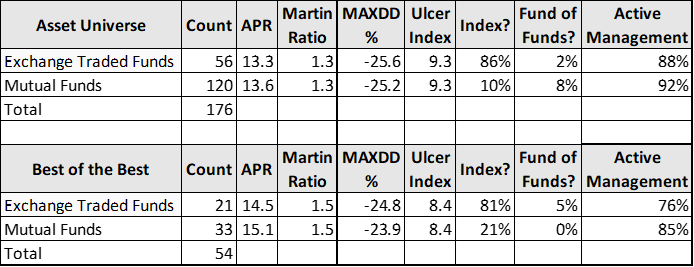

These 176 funds are proven as Annualized % Return (APR) versus Most Drawdown in Determine #2. Clearly some multi-cap funds considerably outperform others. The imply Annualized % Return (APR) over the previous 5 years is 13.5% with 125 (70.6%) mendacity between 11.2% and 15.8% (inside one customary deviation). By comparability, the S&P 500 (SPY) had an APR of 15.9% and a most drawdown of 23.9%. The S&P 500 outperformed 87% of the US Fairness multi-cap funds partly as a result of giant cap development shares carried out so nicely over the previous 5 years.

The pink image in Determine #2 is the median APR and most drawdown. The pink rectangle represents these funds with above-average APR and below-average drawdowns.

Determine #2: Multi-Cap Core Funds APR Versus Most Drawdown (5 Years)

Supply: Creator Utilizing MFO Premium fund screener and Lipper world dataset.

SUMMARY OF TOP PERFORMING MULTI-CAP CORE FUNDS

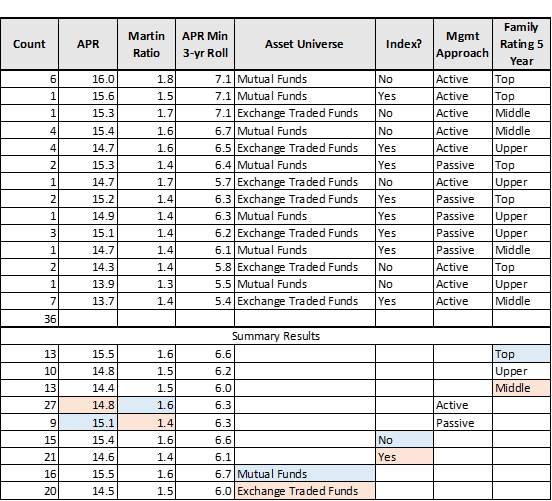

I remove funds with Three Alarm Fund Rankings, above-average Ulcer Rankings, and under common APR, MFO Rankings, Lipper Preservation Rankings, and Fund Household Rankings, in addition to these with very excessive minimal required preliminary investments. This produces fifty-four funds summarized in Desk #4. The refined checklist has a barely larger APR and Martin Ratio (risk-adjusted return) with a barely decrease most drawdown. We are able to conclude that many of the mutual funds should not index funds and use an lively administration method. Many of the trade traded funds are index funds that use an lively administration method.

Desk #4: Multi-Cap Core Funds Universe and Finest Performing (5 Years)

Supply: Creator Utilizing MFO Premium fund screener and Lipper world dataset.

I created a rating system based mostly on APR, Martin Ratio (risk-adjusted return), and APR Minimal 3-year Rolling common to seize a mixture of return, risk-adjusted return, and restoration from downturns. This narrows the checklist right down to thirty-six funds excluding funds that can’t be bought at both Constancy or Vanguard with no price as proven in Desk #5. Typically, I anticipate one of the best funds to be mutual funds that aren’t listed and are managed by the High Fund Households. Passively managed funds are likely to have larger returns whereas actively managed funds are likely to have larger risk-adjusted returns.

Desk #5: Multi-Cap Core Fund Efficiency and Method (5 Years)

Supply: Creator Utilizing MFO Premium fund screener and Lipper world dataset.

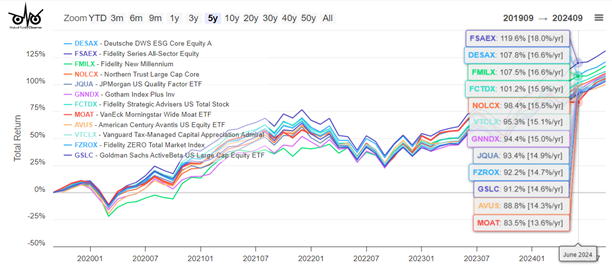

TWELVE TOP PERFORMING MULTI-CAP CORE FUNDS

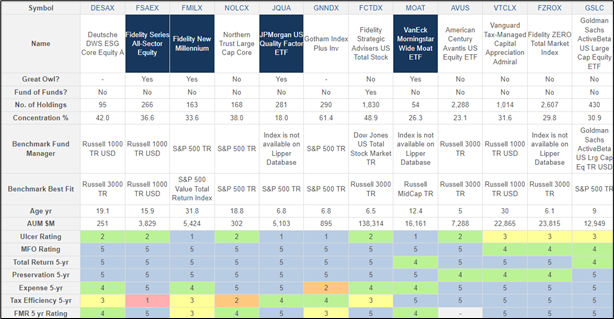

I used my rating system to pick the top-rated funds for APR, Martin Ratio, and APR Minimal 3-year Rolling common proven in Desk #6 and Determine #3. Observe that some funds are much less tax-efficient than others. FCTDX and VTCLX which I personal each present up in my checklist of top-performing multi-cap funds whereas VTI doesn’t.

Desk #6: Twelve High Performing Multi-Cap Core Funds (5 Years)

Supply: Creator Utilizing MFO Premium fund screener and Lipper world dataset.

Determine #3: Twelve High Performing Multi-Cap Core Funds (5 Years)

Supply: Creator Utilizing MFO Premium fund screener and Lipper world dataset.

VALUATIONS MATTER

David Snowball identified final month within the Mutual Fund Observer October 2024 Newsletter that there could be secular bear markets that take greater than ten years for a conventional 60% inventory/40% bond portfolio to get better. Ed Easterling is the founding father of Crestmont Research and writer of Unexpected Returns: Understanding Secular Stock Market Cycles and Probable Outcomes: Secular Stock Market Insights which have a look at the connection of valuations and inflation to those secular bear markets.

There are numerous strategies to outlive these durations equivalent to masking dwelling bills with assured revenue (pensions, annuities, Social Safety), constructing bond ladders, investing for revenue, utilizing a Bucket Method to cowl ten or extra years of dwelling bills in brief and intermediate buckets, variable withdrawal charges to withdraw extra during times with excessive returns and chopping again on discretionary spending throughout years with poor returns. The ultra-wealthy use a method of “purchase, borrow, die” the place they borrow from appreciated belongings as an alternative of promoting them and profit from decrease taxes and the step-up in foundation inheritance legal guidelines.

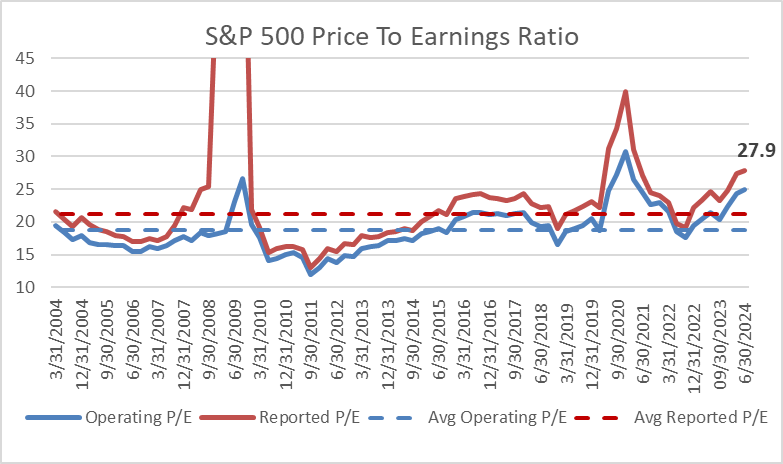

Worth-to-earnings ratios appear easy, however they are often complicated. I produced Determine #4 from the S&P Global knowledge for Working and Reported Earnings per share. The dashed traces are the typical excluding 4 quarters throughout the 2009 monetary disaster that distorted the information. The worth-to-earnings ratios are over 30% larger than the typical of the previous twenty years. The timing of the out there knowledge also can influence the outcomes. Within the following sections, I’ll examine the value to earnings utilizing Morningstar for funds and the S&P 500.

Determine #4: S&P 500 Worth To Earnings Ratio

Supply: Creator Utilizing S&P World

Ed Easterling’s financial physics describes how inflation and valuations drive secular bear markets. Mr. Easterling normalizes the price-to-earnings ratio for the enterprise cycle and concludes:

Right now’s normalized P/E is 40.5; the inventory market stays positioned for below-average long-term returns.

The present valuation stage of the inventory market is above common, and comparatively excessive valuations result in below-average returns. Additional, the valuation stage of the inventory market is very excessive, given the uncertainties related to the at present elevated inflation charge and rate of interest atmosphere…

On this atmosphere, as described in Chapter 10 of Sudden Returns, buyers can take a extra lively “rowing” method (i.e., diversified, actively managed funding portfolio) reasonably than the secular bull market “crusing” method (i.e., passive, buy-and-hold funding portfolio over-weighted in shares).

Constancy invests based on the enterprise cycle as described in How to invest using the business cycle. Vanguard makes use of a low-cost index technique however has a time-varying asset allocation method for its company purchasers. I favor a tilt in direction of bonds as a result of rates of interest and inventory valuations are each excessive.

TAXES MATTER

Excessive nationwide debt has the potential to sluggish financial development and lift borrowing prices. The Congressional Budget Office initiatives that the federal debt held by the general public will rise to 122 % of gross home product by 2034 and that financial development will sluggish to 1.8 % in 2026 and later years. To regulate the nationwide debt, taxes should be elevated, and/or spending equivalent to Social Safety Advantages should be decreased within the coming a long time.

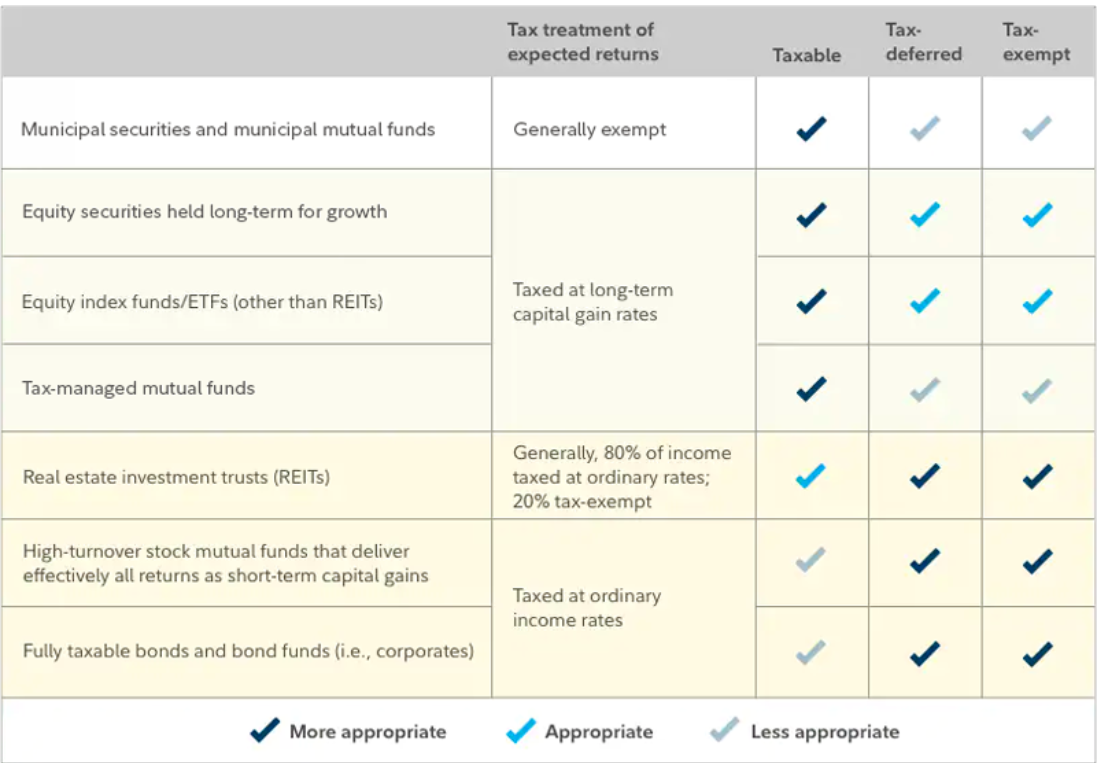

“Are you invested in the right kind of accounts?” by Constancy Viewpoints describes the forms of the forms of accounts, and the significance of asset location to reduce taxes. With regard to multi-cap core funds, funds that maintain equities for long-term development, index ETFs, and tax-managed funds are perfect for buy-and-hold taxable accounts. Multi-cap funds with excessive turnover are higher fitted to Conventional IRAs and Roth IRAs.

Desk #7: Constancy Asset Location and Tax Traits

Supply: Constancy Investments

As a part of monetary planning, I’ve diversified throughout Roth IRAs, Conventional IRAs, and taxable accounts in an effort to have some flexibility with the uncertainty of future tax adjustments. Conventional IRAs have required minimal distributions that are taxed as unusual revenue whereas Roth IRAs don’t. Accounts that use tax loss harvesting can be utilized to assist handle taxes. I favor Roth IRAs as a result of taxes have already been paid, and earnings develop tax-free. Excessive-growth funds and actively managed funds have the potential to generate extra taxable revenue and are typically much less tax-efficient. Concentrating these funds and higher-risk funds in a Roth IRA is good. Tax-efficient multi-cap funds are well-suited for taxable accounts.

AUTHOR’S MULTI-CAP CORE FUNDS

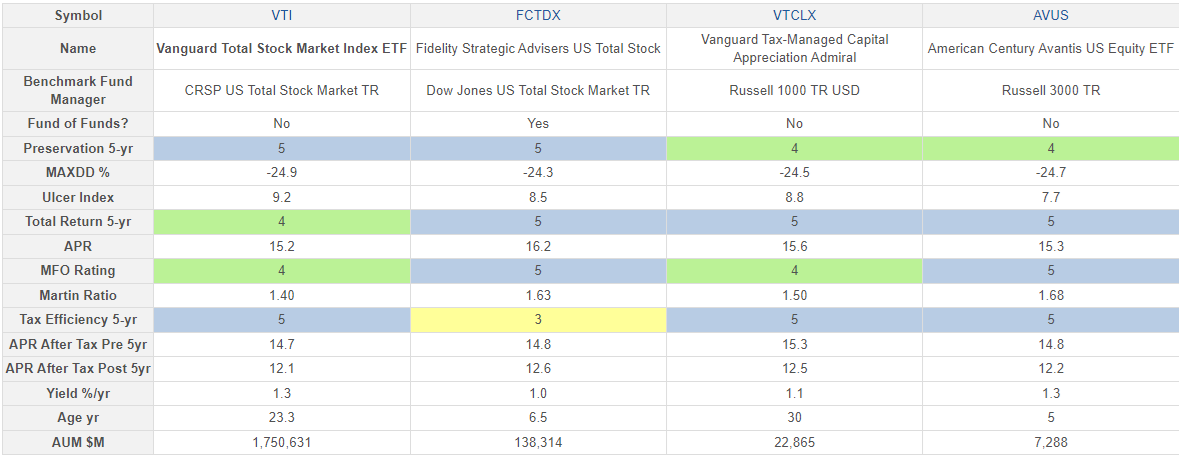

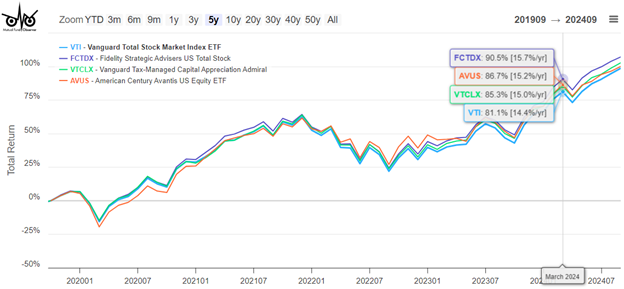

In my professionally managed accounts, Constancy invests in Constancy Strategic Advisers US Whole Inventory (FCTDX) which is just out there to purchasers of Constancy Wealth Providers, and Vanguard invests in Vanguard Whole Inventory Market Index ETF (VTI) whereas I put money into Vanguard Tax-Managed Capital Appreciation Admiral (VTCLX) in a self-managed taxable account. I don’t personal American Century Avantis US Fairness ETF (AVUS) however am within the Avantis funds. All 4 of those funds are top-performing funds.

FCTDX is a fund of funds with excessive returns however isn’t particularly tax environment friendly. It’s perfect for a Roth IRA. VTI additionally has excessive returns and is tax environment friendly and best suited for a taxable account, but in addition suits nicely in a Conventional IRA or Roth IRA. VTCLX is good for a buy-and-hold taxable account.

Desk #8: Creator’s Multi-Cap Core Funds (5 Years)

Supply: Creator Utilizing MFO Premium fund screener and Lipper world dataset.

Determine #5: Creator’s Multi-Cap Core Funds (5 Years)

Supply: Creator Utilizing MFO Premium fund screener and Lipper world dataset.

Strategic Advisers Constancy U.S. Whole Inventory Fund (FTCDX)

Strategic Advisers Constancy U.S. Whole Inventory Fund (FCTDX) is just out there to purchasers enrolled in Constancy Wealth Providers. It outperformed 94% of the multi-cap core funds on this examine. Understanding FCTDX isn’t notably easy. From the Prospectus, I quote a portion of the “Principal Funding Technique” that summarizes the FTCDX finest for me:

The Adviser pursues a disciplined, benchmark-driven method to portfolio building, and screens and adjusts allocations to underlying funds and sub-advisers as essential to favor these underlying funds and sub-advisers that the Adviser believes will present essentially the most favorable outlook for reaching the fund’s funding goal.

When figuring out the right way to allocate the fund’s belongings amongst sub-advisers and underlying funds, the Adviser makes use of proprietary basic and quantitative analysis, contemplating components together with, however not restricted to, efficiency in numerous market environments, supervisor expertise and funding model, administration firm infrastructure, prices, asset measurement, and portfolio turnover.

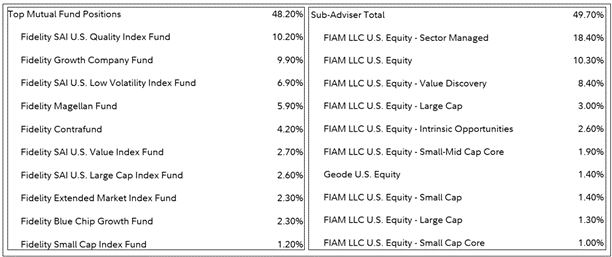

FTCDX is an actively managed fund of funds. Allocations will change based on market circumstances. Present allocations are proven in Desk #9.

Desk #9: FTCDX High Holdings

Supply: Constancy Investments

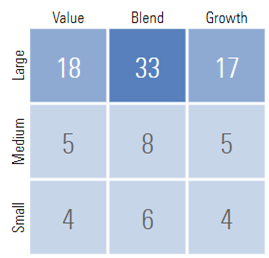

From Morningstar, FCTDX receives 4 stars and a Gold Analyst Ranking. It has a value to earnings ratio of 20.9 in comparison with 22.3 for VTI, and 22.9 for the S&P 500 (VOO). Inventory model weight is proven under:

Desk #10: FCTDX Inventory Type Weight

Supply: Morningstar

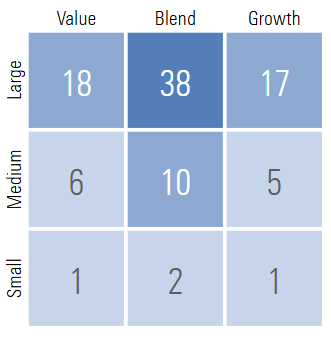

Vanguard Tax-Managed Capital Appreciation Admiral (VTCLX)

Vanguard Tax-Managed Capital Appreciation Admiral (VTCLX) additionally receives a four-star ranking with a Gold Analyst Ranking from Morningstar, “The fund targets shares that pay decrease dividends to boost its tax effectivity whereas additionally mimicking the contours of the flagship Russell 1000 Index, which captures the most important 1,000 US shares.” Its inventory model weights are proven in Desk #11. It has a value to earnings ratio of 21.5. It outperformed 86% of the multi-cap core funds on this examine.

Desk #11: VTCLX Inventory Type Weight

Supply: Morningstar

CLOSING THOUGHTS

The well-known economist, John Maynard Keynes reportedly stated within the 1930’s, “The market can stay irrational longer than you may stay solvent.” Mr. Easterling’s books on secular bear markets satisfied me early on to take care of a margin of security in retirement planning. For me, this meant maximizing contributions to employer financial savings plans, saving extra for extra targets, proudly owning a house, dwelling beneath my means, working past my regular retirement date, rising monetary literacy, and utilizing a Monetary Planner.

On account of writing this text, I’m glad that I’ve top-performing, diversified multi-cap funds that may monitor or beat the entire home markets. I’m comfy that these funds are positioned within the optimum account places. It additionally provides me some concepts to analysis for producing revenue in Conventional IRAs for when required minimal distributions start.