There’s been a number of optimism about mortgage charges below Trump.

In spite of everything, charges have fallen for the previous six weeks from round 7.25% to six.75%, which a reasonably respectable run.

It feels as if the marketing campaign promise to decrease rates of interest wasn’t simply speak, however is definitely actual.

However then whenever you take a look at a mortgage fee chart from when he turned the frontrunner till immediately, it doesn’t look as nice.

In reality, it appears like we’ve gone nowhere in any respect, whereas the financial system now feels loads shakier.

Mortgage Charges Are Merely Again to Pre-Election Ranges

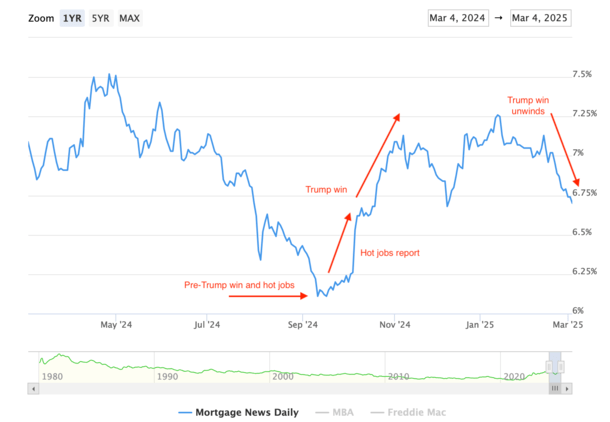

I annotated a mortgage fee chart from Mortgage News Daily to make my case.

By the best way, this isn’t political, it’s merely wanting on the timeline and the numbers.

If we return to September, the 30-year fastened was at its lowest level in a number of years, hovering simply above 6%.

That was really fairly good on the time, and was pushed by the Fed pivot, by which they cease climbing and sign a future reduce.

Once they lastly did reduce, mortgage rates bounced a bit of larger. Not by a lot, however type of a promote the information occasion.

In different phrases, everybody knew the Fed was going to chop, and as soon as they lastly did, charges didn’t fall.

They didn’t fall as a result of the rumor of a Fed fee reduce, which is very telegraphed, was already baked in.

Shortly after the Fed reduce, a hot jobs report got here down the pipe. This was unlucky timing, and obtained muddled with the Fed fee reduce.

A lot in order that it appeared that mortgage rates jumped after the Fed cut rates. Everybody was baffled.

However in the end, the roles report was the difficulty, not the Fed fee reduce. Whereas the Fed doesn’t control mortgage rates, a fee or a hike shouldn’t make that a lot of an impression.

And it didn’t. It was the roles report, which resulted within the 30-year fastened surging about 25 foundation factors (0.25%) in sooner or later.

Mortgage Charges Rise as Trump Turns into the Frontrunner to Win the Election

Shortly after these two huge occasions, a 3rd huge occasion surfaced in fast succession. A Trump presidential victory turned an apparent favourite.

It wasn’t a executed deal, however the odds of Trump profitable the election started to get baked into mortgage charges too.

And by that, I imply mortgage charges started rising much more. In spite of everything, a lot of his proposed insurance policies had been/are anticipated to be inflationary.

Issues like tariffs, deportations, tax cuts, elevated authorities spending. So the 30-year fastened then climbed one other 50 bps.

From round 6.625% to 7.125%, whereas additionally breaching the all-important 7% psychological barrier.

It was yet one more gut-punch for debtors trying to refinance, potential first-time home buyers, and the various who work within the mortgage and actual property business.

At its worst, the 30-year fastened hit 7.25%, simply across the time Trump was inaugurated, coincidence or not.

For the file, the identical factor occurred in late 2016 when Trump received. The 30-year fastened rose from round 3.50% to roughly 4.30%. A full 80 bps improve.

So in a way, this wasn’t in any respect sudden, and a number of the improve really befell earlier than the election as a substitute of merely after this time round.

Bessent Offers Mortgage Charges a Push Again to The place They Began

As soon as Trump obtained into workplace, the 30-year fastened started falling. As for why, it was largely a reversal of what was baked in main as much as the inauguration, maybe prematurely and with out justification.

And charges had been capable of ease due to dovish speak from newly-appointed Treasury Secretary Scott Bessent.

Just about all of his feedback relating to rates of interest have been about pushing them lower since mid-January.

The market has gotten on board with it, primarily as a result of issues like tariffs and tax cuts haven’t been as dangerous as anticipated (but).

We’ve additionally acquired cooler financial knowledge since then, which has helped mortgage charges return to these pre-election ranges as properly.

On the similar time, the inventory market has roughly returned to the lower levels seen again in September.

And that has been accompanied by a flight to security in bonds, which track mortgage rates really well.

The ten-year yield was as low as 3.65% in September earlier than leaping to 4.10% after that scorching jobs report, after which climbed even additional to round 4.80% by the point Trump entered workplace.

It’s now nearer to 4.25%, which is just a bit bit above the degrees seen after the September jobs report.

So once more, we’ve largely simply come full circle. Certain, mortgage charges may have saved rising after Trump obtained into workplace, however they didn’t.

We will take that as a win, but it surely’s vital to have context right here. Mortgage charges have moved decrease up to now couple months, however nonetheless stay properly above ranges seen final September.

They usually’re just about according to ranges seen a 12 months in the past, which can or might not do a lot for potential residence patrons getting into the spring housing market.

Particularly if residence purchaser sentiment has soured because of larger uncertainty surrounding the financial system.

That’s the kicker – charges have moved down these days, however largely as a result of the financial outlook has worsened tremendously. It’s bittersweet.

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on X for warm takes.