These days, I’ve been highlighting mortgage applications past the 30-year mounted now that rates of interest on fixed-rate mortgages are not favorable.

At this time, we’ll examine two in style loan programs, the 30-year mounted versus the 7-year ARM.

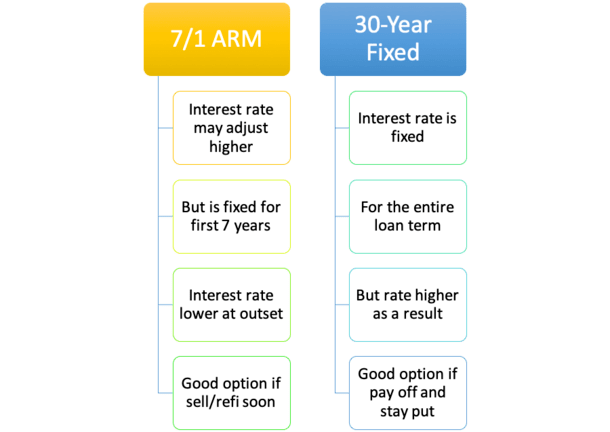

Everyone seems to be conversant in the standard 30-year fixed – it’s a house mortgage with a 30-year time period and an rate of interest that by no means adjusts your entire mortgage time period. Fairly easy, proper?

However what concerning the 7-year ARM, or extra particularly, the 7/1 ARM? It’s an adjustable-rate mortgage and a fixed-rate mortgage, all rolled into one. Sounds somewhat bit extra difficult…

Let’s dig in and decide if it’s time to start out trying past the 30-year mounted to probably avoid wasting cash on your private home mortgage.

Key Info About 7-12 months ARMs

- They’re hybrid dwelling loans which might be mounted for 7 years and adjustable for the remaining 23 years

- Provide an rate of interest low cost for the danger of future (increased) price changes

- 7/1 ARM is mounted for seven years and yearly adjustable thereafter

- 7/6 ARM is mounted for seven years and adjusts each six months thereafter

- Take note of the distinction in begin price to find out if it’s price it vs. a 30-year mounted

- Plan for the worst seven years from date of mortgage funding (if charges leap rather a lot increased)

How the 7/1 ARM Works

- You get a set rate of interest for the primary seven years of the mortgage time period

- After that the speed turns into yearly adjustable for the remaining 23 years of the 30-year mortgage time period

- Many debtors don’t hold their mortgage/dwelling that lengthy so chances are you’ll by no means really face a price adjustment for those who refinance or promote previous to seven years

- It’s an choice to contemplate alongside the extra in style 30-year mounted now that mortgage charges are not on sale

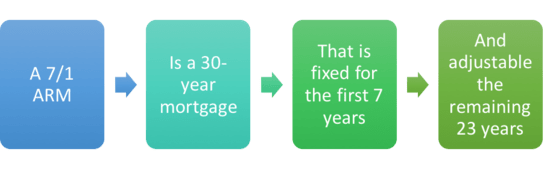

A 7/1 ARM is an adjustable-rate mortgage with a 30-year time period that contains a mounted rate of interest for the primary seven years and a variable price for the remaining 23 years.

Let’s break it down. In the course of the first seven years of the mortgage time period, the mortgage rate is mounted, which means it gained’t change from month-to-month, and even year-to-year.

So if the beginning rate of interest is 6%, that’s the place it should stay till it’s first adjustment in month 85.

For all intents and functions, the mortgage program provides debtors a set price for a really prolonged 84 months.

In the course of the remaining 23 years, the speed is adjustable, and might change simply as soon as per yr. That’s the place the quantity “1” in 7/1 ARM is available in.

This makes the 7-year ARM a so-called “hybrid” adjustable-rate mortgage, which is definitely excellent news.

You basically get one of the best of each worlds. A decrease rate of interest due to it being an ARM, and a protracted interval the place that price gained’t change.

It affords you two further years of mounted funds when in comparison with the 5/1 ARM. And people 24 additional months may turn out to be useful…

You May Additionally Come Throughout the 7/6 ARM

These days, extra mortgage lenders have been pitching ARMs that modify each six months as an alternative of yearly.

So chances are you’ll come throughout a “7/6 ARM,” which because the identify implies is mounted for the primary seven years after which adjusts twice every year (each six months) thereafter.

The excellent news is it’s not all that totally different than the 7/1 ARM. You continue to get the seven years of mounted price goodness, which is arguably an important function.

Then you definitely’re topic to a price adjustment each six months. For those who nonetheless have your ARM at that time, you may discover a refinance if charges are favorable.

In any other case, you’ll have to deal with extra changes (two every year as an alternative of 1), although it needs to be famous that charges can transfer each up and down.

For those who want one mortgage kind over the opposite, store accordingly to see which lenders supply the 7/1 ARM vs. the 7/6 ARM, or vice versa.

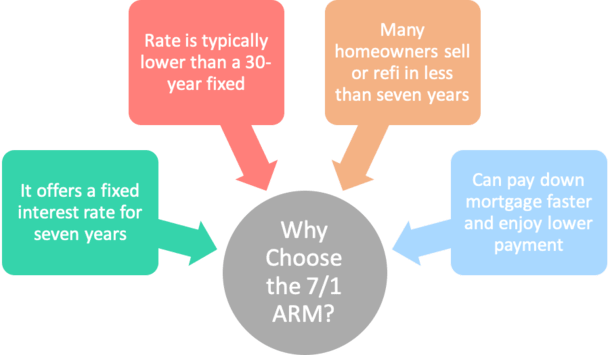

Why Select the 7/1 ARM?

- You may acquire a decrease rate of interest (and month-to-month fee) for a protracted time period

- Could be considerably cheaper relative to accessible fixed-rate mortgage choices

- This mortgage kind nonetheless contains a mounted rate of interest for a full seven years

- That means chances are you’ll successfully maintain a fixed-rate mortgage for so long as you personal your private home or till you refinance

You most likely don’t need your mortgage price (and mortgage payment) to alter on a regular basis, particularly in case your price will increase, which might be the likelier end result.

With the 7/1 ARM, you get mortgage price stability for a full seven years earlier than even having to fret concerning the first price adjustment.

And since most householders both promote or refinance earlier than that point, it may show to be a sensible choice for these on the lookout for a reduction.

That’s proper, 7/1 ARM mortgage charges are cheaper than the 30-year mounted, or at the least they need to be.

By cheaper, I imply it comes with a decrease rate of interest than the 30-year mounted, which equates to a decrease month-to-month mortgage fee for the primary 84 months!

As famous, most householders don’t hold their dwelling loans that lengthy anyway, so there’s an honest likelihood the borrower won’t ever see that first adjustment, but nonetheless get pleasure from that low price month after month for years.

How A lot Decrease Are 7/1 ARM Charges vs. the 30-12 months Fastened?

On the time of this writing, mortgage charges on the 7-year ARM are being supplied at round 6%, whereas the everyday price on a 30-year mounted is about 6.75%.

[What mortgage rate can I expect?]

That’s an OK price unfold, particularly after a protracted interval the place fixed-rate mortgages have been really cheaper than ARMs.

This unusual phenomenon came about as a result of the Fed pledged to purchase up long-term fixed-rate mortgage securities, driving mortgage charges down within the course of (it was generally known as QE).

As such, ARMs weren’t providing a lot of a reduction (if any) and sometimes weren’t even price trying into usually.

However in regular instances, which we’re beginning to return to, you may discover an excellent wider unfold between the 2 merchandise.

For instance, a number of years again the 7-year ARM averaged 3.64%, whereas the typical price on a 30-year mounted was 4.69%.

That resulted in a month-to-month fee distinction of $122.28 a month, $1,467 per yr, and over $10,000 over the primary seven years on a $200,000 mortgage quantity. Not dangerous, eh?

I’ve additionally come throughout 7/1 ARM charges as little as 5.375% recently, which might signify a distinction of 1.375% versus a comparable 30-year mounted at 6.75%.

Let’s Calculate the Potential Financial savings of a 7/1 ARM

| $300,000 Mortgage Quantity | 7/1 ARM | 30-12 months Fastened |

| Mortgage Price | 5.375% | 6.75% |

| Month-to-month P&I Fee | $1,679.91 | $1,945.79 |

| Whole Price Over 60 Months | $100,794.60 | $116,747.40 |

| Remaining Steadiness After 84 Months | $265,808.29 | $272,362.94 |

| Whole Financial savings | $22,507.45 |

Think about you’re capable of finding a 7/1 ARM at a price of 5.375% as an alternative of a 30-year mounted at 6.75%.

That’s a giant distinction in price, affording you a month-to-month fee that’s about $266 much less monthly.

Not solely would you lower your expenses long-term, however you’d additionally save month-to-month, which means you can put that more money to good use elsewhere, corresponding to in a extra liquid funding.

Or just set it apart to pay different payments (like high-interest bank cards) or construct up an emergency fund.

The decrease price would additionally pay down your principal steadiness sooner, which means you’d accrue dwelling fairness sooner.

To that finish, your remaining steadiness after 84 months could be about $6,500 decrease with the ARM.

Taken collectively, you’d be greater than $22,500 forward after seven years due to a smaller excellent mortgage steadiness and decrease month-to-month fee.

Are the Decrease 7/1 ARM Charges Well worth the Danger?

- It’s important to weigh the danger and reward of the 7/1 ARM

- When you obtain a reduced rate of interest for a prolonged seven years

- Maybe .50% to .625% decrease than the 30-year mounted throughout regular instances

- Take into account the danger of the speed adjusting increased in yr 8 and past until you promote your private home or refinance earlier than that point

Now let’s discuss threat. As famous, 7/1 ARM charges are usually cheaper than the 30-year mounted, however how a lot is determined by the present price surroundings.

I’ve discovered less expensive charges at credit score unions (an excellent place to look if you’d like an ARM!), however many larger lenders and banks may solely supply a .50% low cost.

At that time, the financial savings could not justify the danger of a better price after first adjustment.

For those who really plan on staying in your house and paying off your mortgage, you face the opportunity of an rate of interest reset (increased, or maybe decrease) sooner or later.

And also you don’t wish to get caught out if mortgage charges surge over the subsequent seven years, particularly for those who can’t promote your private home or don’t wish to.

Nonetheless, for those who’re like many People, who promote or refinance the mortgage inside seven years, the mortgage program may make a whole lot of sense.

However you’re nonetheless timing the market to some extent, hoping it’s an excellent time to promote sooner or later, or that refinance charges are enticing throughout these 84 months.

Evaluate Charges/Prices to the 30-12 months Fastened. Do the Math

Simply make sure you do the maths on each eventualities earlier than committing to both of those mortgage applications.

Generally the speed unfold between seven-year ARM charges and the 30-year mounted isn’t that broad.

For the time being, the unfold is starting to widen, making adjustable-rate mortgages favorable once more.

Nonetheless, you do have to put in additional to buy round as a result of ARM charges can differ much more from financial institution to financial institution than mounted charges.

For those who put within the legwork, chances are you’ll discover a financial institution or lender prepared to supply a extra substantial low cost.

For instance, credit unions tend to offer lower ARM rates and will supply a wider unfold versus the competitors, particularly banks and massive family lenders.

Regardless, this unfold can and can fluctuate over time, so all the time take the time to contemplate that when making a call between the 2 mortgage applications.

Clearly, the upside is diminished and it will get riskier if the 2 mortgage applications are pricing equally.

Make Positive You Can Afford the 7/1 ARM After It Resets

- It is perhaps clever to have a look at the worst-case situation

- Which is the utmost rate of interest your mortgage can modify to

- This ensures you may deal with the bigger month-to-month mortgage funds

- Assuming you don’t promote or refinance or are unable to and your price adjusts considerably increased

Additionally be aware that it is best to be capable to afford the fully-indexed price on a mortgage ARM, ought to it modify increased.

After these seven years are up, the rate of interest can be calculated utilizing the margin and the index price (corresponding to SOFR) tied to the mortgage. This price may very well be significantly increased than what you have been paying.

In different phrases, anticipate and plan for price will increase sooner or later and be sure you can take in them if for some purpose you don’t promote your private home or refinance your mortgage first.

If a price adjustment isn’t inside your price range, or gained’t be sooner or later when it adjusts, chances are you’ll wish to pay it protected with a fixed-rate mortgage as an alternative of the 7/1 ARM.

Imagine it or not, seven years can go by fairly quick.

Refinancing Your 7-12 months ARM within the Future

The excellent news is even when mortgage charges are increased seven years after you’re taking out your mortgage, you’ll nonetheless be fairly far forward from all of the financial savings realized throughout that point.

You’ll have a smaller excellent mortgage quantity due to extra of your month-to-month fee going towards the principal steadiness and also you’ll have saved a ton on curiosity.

So even when refinance charges are increased sooner or later, otherwise you merely let it journey with a price adjustment, you should still come out forward, at the least for a short time.

If nothing else, the financial savings in the course of the first seven years could provide you with respiratory room to pay extra sooner or later, or refinance at extra enticing phrases.

In abstract, the 7-year ARM may not be for the faint of coronary heart, whereas a 30-year mounted is fairly simple and stress-free. And that’s why you pay extra for it.

For those who’re sure you gained’t be staying in a property for greater than 5 or so years, it may very well be a strong different and a giant cash saver if spreads are broad.

To know for certain, use a mortgage calculator to match the prices of every mortgage program over your anticipated tenure within the property.

7/1 ARM Ceaselessly Requested Questions

What’s the 7/1 ARM price immediately?

Charges differ significantly by financial institution, lender, and credit score union, and by your particular person mortgage situation. However you will get a really feel for charges by looking out lender price pages.

I’ve discovered that the bottom 7/1 ARM charges are supplied by native credit score unions. Seek for one in your metropolis or state and examine it to the nationwide banks and lenders to see what I imply.

Are you able to refinance out of a 7/1 ARM at any time?

Sure, so long as you qualify for the mortgage. A refinance isn’t a lot totally different than a house buy mortgage. You’ll nonetheless have to qualify based mostly on revenue, employment, credit score rating, and so forth.

If charges drop and/or your first adjustment is imminent, you may look right into a refinance to safe a brand new fixed-rate time period on an ARM or go along with a fixed-rate mortgage.

For instance, you may refinance into one other 7/1 ARM or a 30-year mounted.

How lengthy does the 7/1 ARM final?

Regardless of it being referred to as a 7-year ARM, it’s a 30-year mortgage identical to the 30-year mounted. Nonetheless, the seven refers back to the mounted price interval, which is barely the primary seven years, or 84 months.

The remaining 23 years of the mortgage are adjustable, both as soon as yearly within the case of the 7/1 ARM, or biannually within the case of the 7/6 ARM.

What occurs when the 7-year ARM expires?

After seven years, the speed is not mounted and turns into adjustable.

To find out your rate of interest, the lender makes use of the mix of your margin (test your mortgage paperwork for this quantity) and the corresponding mortgage index.

Collectively, these two figures make up your fully-indexed price. And each six or 12 months, the lender will modify your price based mostly on modifications to the index. The margin is all the time mounted.

For instance, if the margin is 2.5% and the index is 4.75%, the speed could be 7.25%.

On the subsequent adjustment, if the index rises to five%, the brand new price could be 7.50%.

Is there a penalty for paying off an ARM early?

Typically, no. Prepayment penalties have been quite common within the early 2000s, however very unusual immediately. However all the time ask to make certain.

If there isn’t any penalty, you may refinance or promote at any time with out paying any type of early payoff charge.

How a lot can a 7/1 ARM go up?

It is determined by the ARM caps, which dictate motion every adjustment interval. Usually, you’re 2% caps every adjustment interval and maybe 5% max for the lifetime of the mortgage.

That’s nonetheless sizable, which means in case your begin price have been 5.5%, the speed may probably go to 10.5%!

Is the 7/1 ARM a good suggestion proper now?

It’s definitely changing into extra compelling with fixed-rate mortgages so costly relative to some years in the past.

But it surely relies upon how a lot decrease the speed is, what your plan is for the property (anticipated holding interval), rate of interest outlook, and so forth.

Finally, you take a threat with an ARM and wish a plan for all attainable eventualities.

7/1 ARM Execs and Cons

The Good

- You get a set rate of interest for a whole seven years (84 months!)

- The speed is usually a lot decrease than a 30-year mounted

- Extra of every month-to-month fee will go towards the principal steadiness as an alternative of curiosity

- Most householders transfer or refinance in much less time than that

- So you may get pleasure from a decrease mortgage price with out worrying a couple of price adjustment

The Unhealthy

- It’s an ARM that may modify increased after seven years

- Month-to-month funds could turn into rather more costly for those who maintain onto it

- The rate of interest low cost is probably not definitely worth the threat of the speed adjustment

- Extra stress for those who maintain the mortgage wherever close to seven years

- May very well be caught with the mortgage if unable to promote/refinance as soon as it turns into adjustable

Learn extra: 30-year fixed vs. 15-year fixed.

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) dwelling patrons higher navigate the house mortgage course of. Observe me on X for warm takes.