With so many requires larger mortgage charges recently, now could be the right time to play contrarian.

It’s one thing I love to do basically, however it appears to work even higher when the topic is “mortgage charges.”

Usually when the consensus is excessive, issues are likely to unexpectedly shift and shock everybody.

In the intervening time, everyone seems to be within the higher-for-longer camp, a lot in order that it appears they’ll’t all be proper.

And when it looks like there’s completely no hope in sight, the storm clouds half.

A lot of Headwinds for Mortgage Charges Proper Now

In the intervening time, it looks like mortgage charges are using a bicycle with a flat tire up a steep hill within the pouring rain.

Nothing appears to be going their method, whether or not it’s tariffs, the commerce battle, the large, stunning invoice (and all that authorities spending), the U.S. credit rating downgrade, and now even talks about Fannie and Freddie being released.

All of this stuff are contributing to higher bond yields, which directly impact long-term fixed mortgage rates.

The ten-year bond yield has risen markedly over the previous three weeks, climbing from round 4.15% to 4.55% right this moment.

It was as excessive as 4.60% yesterday, however has since cooled off. Nonetheless, that’s sufficient to place the 30-year fastened firmly again above 7% because of bloated spreads.

And each time the 30-year fastened climbs again above 7%, you may simply really feel the wind exit of the housing market’s sails.

The month-to-month fee distinction isn’t large, however the shift in sentiment in palpable.

Nevertheless, what if I advised you mortgage charges would possibly nonetheless be on monitor to enhance by later this yr.

And that instances like these are once we are most stunned?

Again to my contrarian level, it’s when a commerce will get crowded that issues are likely to unravel. When everyone seems to be so certain of one thing, on this case larger mortgage charges, they go the opposite method.

Zoom Out on Mortgage Charges for a Clearer Image

I all the time wish to zoom out a bit when talking of mortgage charges. An excessive amount of can occur on a day-to-day foundation, just like the inventory market.

Sure, mortgage rates can change daily, however it’s vital to take a look at the longer trajectory for solutions.

Simply contemplate this chart from Mortgage News Daily for the previous 24 months. There’s a clear downward slope in mortgage charges, regardless of the latest volatility and upward motion.

There additionally tends to be an increase in mortgage rates every spring, which additionally occurs to be the height residence shopping for season (go determine).

In the meantime, mortgage rates tend to be lowest in winter when issues are the slowest (additionally go determine).

That smartened me up for my 2025 mortgage rate predications post, the place I made the adjustment for larger charges within the second quarter, earlier than forecasting a transfer decrease in Q3 and This autumn.

My prediction continues to be in play and going in accordance with plan, although it could be a bit delayed based mostly on the numerous occasions which have taken place.

The Fed Is Staying the Course because the Drama Performs Out, Knowledge Is What Issues

There have been a number of surprises (and fireworks) up to now in 2025, however on the identical time we have been warned about all of this.

Everybody knew Trump winning the election would result in tariff talk, commerce wars, elevated authorities spending, and so forth.

Even the considered Fannie and Freddie leaving conservatorship was within the playbook.

When it comes right down to it, none of this comes as a significant shock. Everybody was advised this stuff have been going to occur, so you may’t be all that shocked.

This additionally explains why the Fed has been enjoying a gradual hand, as a substitute of panicking and slicing charges forward of schedule.

Nevertheless, they’re nonetheless anticipated to chop, it’s simply that the Fed charge cuts have been pushed out.

The identical basic outlook exists, a cooling economic system with rising unemployment, which ought to result in decrease bond yields and charge cuts.

It’s simply that due to all of the drama and the months of commerce wars, and the brand new tariffs, it’s unclear what the information will appear like for a short time.

Likelihood is it’ll present elevated inflation. However how a lot of it? And can it’s sufficient to spark a return to eight% mortgage charges?

I watched a video from JPMorgan Asset Administration fastened earnings portfolio supervisor Kelsey Berro and she or he did a superb job placing every part in perspective.

She famous that the vary for the 10-year bond yield is 3.75% to 4.50%, with short-term dangers pushing charges larger, however longer-term, we’re already on the larger finish of the vary.

Which means we’re already capped out factoring in all of the stuff occurring for the time being.

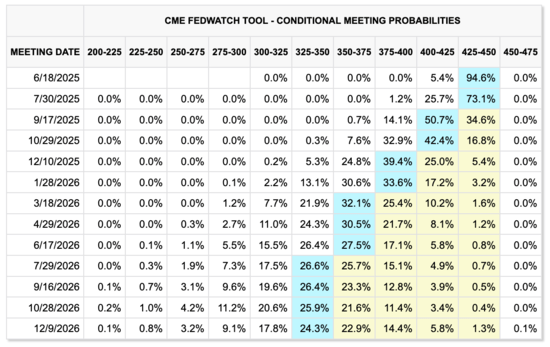

One in every of her largest takeaways was that “The Fed continues to be in a impartial to easing bias.” There aren’t any charge hikes on the desk.

The truth is, should you have a look at the CME FedWatch chance chart above, there’s a 0.0% probability of a charge hike from now by means of the top of October 2026. And solely a 0.1% probability by the top of 2026.

She added that a few of the new authorities finances has already been priced in to the lengthy finish of the yield curve.

So it’s not like mortgage charges must hold going as much as compensate if it’s already baked in.

Keep in mind, we have been very near a 6% 30-year fastened final September, and at the moment are at 7.125% as of this writing.

Mortgage charges ARE already larger to compensate.

In the meantime, the economic system continues to indicate indicators of weak point and in the end the way forward for charges will depend upon that very inflation and financial information.

Which may clarify why Fannie Mae’s newest projection launched yesterday has the 30-year fastened falling to an excellent decrease 6.1% by the top of 2025 and 5.8% in 2026.

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) residence consumers higher navigate the house mortgage course of. Comply with me on X for warm takes.