It’s been a very good couple of weeks for mortgage charges, which benefited from a delay on tariffs and a few favorable financial knowledge.

Between a slowing financial system, diminished inflation, and the thought that the tariffs may very well be overblown, the 10-year bond yield has improved markedly.

Since hitting its 2025 excessive of 4.81% on January thirteenth, it has since fallen a large 35 foundation factors in lower than a month.

This has been pushed by cooler inflation/financial knowledge and fewer concern of tariffs and a wider commerce battle.

Nevertheless, mortgage charges haven’t fallen by the identical quantity, which tells you there’s a nonetheless a number of defensiveness on pricing.

Mortgage Lenders Stay Defensive on Pricing

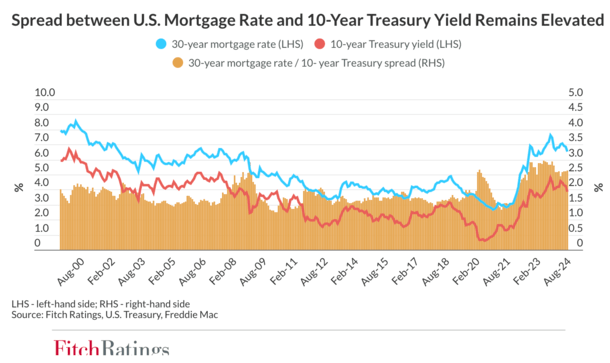

The 10-year bond yield is a good way to track mortgage rates, with the 30-year fastened transferring in relative lockstep over time.

Nevertheless, over the previous couple years mortgage rate spreads (the premium MBS buyers demand) have risen significantly.

Over a lot of this century, since no less than the 12 months 2000, the unfold has hovered round 170 foundation factors on common.

Throughout late 2023, it widened to round 300 foundation factors (bps), that means buyers demanded a full 3% unfold above comparable Treasuries, as seen within the chart above from Fitch Ratings.

This was largely pushed by prepayment danger, and to a point credit score danger, resembling mortgage default.

However my guess is it has been principally prepayments that MBS buyers concern, as a result of mortgage rates practically tripled in a couple of 12 months’s time.

In different phrases, the thought was these mortgages wouldn’t have a lot of a shelf life, and could be refinanced sooner moderately than later.

The unfold has since are available a bit, however remains to be round 260 bps, that means it’s practically 100 bps above its long-term common.

Merely put, pricing stays very cautious relative to the norm, and it has gotten worse over the previous couple weeks.

The spreads had been truly making their means nearer to the decrease 200 bps-level earlier than climbing once more not too long ago.

Is There Too A lot Volatility for a Flight to Security?

As for why, I’d guess elevated uncertainty and volatility. In spite of everything, each Canada and Mexico confronted tariffs final week earlier than they had been “delayed.” However the tariffs on China are nonetheless in impact.

Whereas the market typically cheered this growth, who’s to say it doesn’t flip-flop in every week?

The identical goes for all the federal government businesses being suspended or shut down, or the buyouts given to federal staff.

For lack of a greater phrase, there may be a number of chaos on the market in the meanwhile, which doesn’t bode properly for mortgage charges.

They are saying there’s a flight to security when the inventory market and wider financial system is unstable or risky, the place buyers ditch shares and purchase bonds.

This will increase the worth of bonds and lowers their yield, aka rate of interest. That is good for mortgage charges too primarily based on the identical precept.

However there comes a sure level when circumstances are so risky that each bonds and shares grow to be defensive on the identical time.

Each can unload and no one actually advantages, with customers seeing the wealth impact fade whereas additionally dealing with increased rates of interest.

[Mortgage rates vs. the stock market]

The 30-Yr Fastened Might Be within the Low 6s Immediately

The large query is when can we see some stability within the bond and MBS market, which might permit spreads to lastly are available?

Some say the 10-year yield at round 4.50% right now is pretty cheap given present financial circumstances.

If that’s going to kind of keep put, the one different option to get mortgage charges decrease is via spread compression.

We all know the spreads are bloated and have room to come back down, in order that’s what might be wanted barring a contracting financial system or a lot worse unemployment driving yields decrease.

Assuming the spreads had been even near their current norms, say 200 foundation factors above the 10-year, we’d have already got a 6.5% 30-year fastened. Even perhaps a 6.375% charge.

Those that opted to pay discount points might seemingly get a charge that began with a “5” and that wouldn’t be half dangerous for many new house patrons.

It might even be fairly interesting for many who bought a house in late 2022 by way of 2024, who may need an rate of interest of say 7 or 8%.

In different phrases, there’s a ton of alternative only a tighter unfold away. Plenty of the heavy lifting on combating inflation has already been executed.

So if we are able to get there, borrower reduction is on the best way. And mortgage lenders which have been treading water and barely surviving these previous few years will presumably be saved as properly.

We simply want clearer messaging and coverage from the brand new administration, which can permit buyers to exit their overly-defensive stance.

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) house patrons higher navigate the house mortgage course of. Comply with me on Twitter for decent takes.