I noticed his seemingly simple query posed and was shocked I’d by no means actually addressed it.

I’ve been writing about mortgages on this weblog since 2006, so likelihood is I’ve lined most issues.

However I hardly ever assume when it comes to a mortgage being a alternative. For many, it’s obligatory, given how costly houses are as of late.

Few should purchase a property with money, so the mortgage is commonly a given after we’re discussing a house buy.

That being stated, we are able to talk about the professionals and cons of getting a mortgage (and maintaining it long run).

Fairly A lot Everybody Wants a Mortgage

First issues first. In case you’re studying this and wish to purchase a house (or already personal a house), likelihood is you both want a mortgage or have one.

It’s just not practical to buy a home with cash for almost all of the inhabitants.

Your common American can’t even muster a 20% down payment, so the possibilities of them shopping for a house outright is slim.

However past that, even those that can afford to purchase a house with money usually don’t. simply have a look at Beyoncé or Mark Zuckerberg.

When given the prospect, they nonetheless opted for a mortgage. Why? As a result of financing is commonly a greater play than locking up all their money in an illiquid investment.

Their cash is put to raised use (theoretically) in different investments, whether or not it’s the inventory market or one thing else.

All they really want to do is earn a charge of return larger than the rate of interest on their mortgage.

On prime of that, they get the bonus of diversification. Do you actually need all or loads of your cash tied up in a single factor? A house, which is prone to danger, equivalent to a wildfire or a flood.

You’ve heard the phrase “don’t put your eggs in a single basket,” and this is applicable to actual property too.

Is It Higher to Be Mortgage-Free?

Okay, so we all know each wealthy and not-so-rich usually go for a house mortgage as an alternative of paying money for a property.

However is it higher to be mortgage-free, that means finally paying off the mortgage and holding a free and clear property?

One might argue that for the typical individual, sure, you need to finally repay your mortgage.

In spite of everything, you’re paying plenty of curiosity every month and principal, and it’s doubtless an costly a part of your month-to-month nut.

In case you can take away the mortgage out of your checklist of liabilities, you’ll have much more money readily available for different bills or investments.

And also you received’t be paying a ton of curiosity to the financial institution each month anymore, which is arguably a superb factor.

That is very true should you’re at/near retirement, as it’s generally recommended not to take a mortgage into retirement should you’ll be on a hard and fast revenue.

Nevertheless, there’s a giant distinction between paying off the mortgage and prepaying the mortgage.

The latter means you might be voluntarily and actively CHOOSING to allocate extra of your cash to the mortgage every month.

If that is so, it is advisable think about the mortgage rate as your charge of return for making that aware “funding.”

What About Owners with 2-4% Fastened-Fee Mortgages?

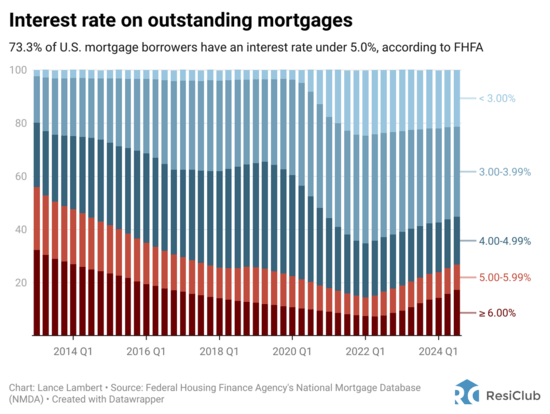

Let’s think about that repay vs. prepay query for a second. As we speak, nearly all of householders have a mortgage charge beneath 5%.

Ultimately look, it’s one thing like 75% of mortgage holders have charges under 5%. And about 40% have a charge under 4%, per FHFA data compiled by Lance Lambert.

Many tens of millions extra have charges within the 1-3% vary. Sure, charges that begin with 1%. This can be a distinctive phenomenon associated to the Fed’s Quantitative Easing (QE) program, which has since closed.

That entailed shopping for trillions in mortgage-backed securities (MBS) to drive mortgage charges decrease.

So in right now’s day and age, householders doubtless view mortgages quite a bit otherwise than they did up to now.

The long-term average for the 30-year fixed is around 7.75%, and everyone knows mortgages rates in the 1980s hit 18%.

This implies the argument to take out and preserve a mortgage is night time and day in comparison with these days.

In case you speak to an older house owner, they could nonetheless be biased to pay it off as rapidly as potential.

However should you speak to a youthful house owner, they could say what’s the push? I wish to preserve this factor so long as potential.

In different phrases, context issues and it is advisable have a look at your rate of interest and mortgage kind to make this willpower.

There isn’t a common mortgages are unhealthy or mortgages are good reply. Like most issues, it relies upon.

The house purchaser right now who can solely get a 7% mortgage might need a very completely different view of mortgages, and for good cause.

Personally, I am debt-averse, that means I don’t like to hold any debt, however I’m pro-mortgage and imagine mortgage is generally a good debt.

Assess the State of affairs to Decide If a Mortgage Is Proper for You

As famous, most of us NEED a mortgage. It’s not even a query you’ll weigh when shopping for a house since you received’t have some other choice.

Nevertheless, you’ll nonetheless have the choice to pay off your mortgage ahead of schedule. So that’s one thing to think about as soon as you are taking out a mortgage.

The reply to that query will doubtless rely on what kind of mortgage you might have and what your rate of interest is.

As a common rule of thumb, these with fixed-rate mortgages set at very low rates of interest will wish to preserve their loans longer, probably to maturity.

Conversely, these with higher-interest charge loans might want to sit down and think about prepaying them, assuming they’ll’t earn extra money elsewhere, equivalent to in a retirement account.

There isn’t any one-size-fits-all answer, so that you’ll must put within the time and do the mathematics to make this willpower. You may even think about a monetary planner to help you with this query.

The Execs and Cons of Having a Mortgage

The Good

- Mortgages are low-cost debt relative to different choices

- Can get a hard and fast charge over a protracted time frame (30-year mounted)

- Can help you put little down on a house buy

- Creates diversification of belongings with cash obtainable for different investments

- Requires householders insurance coverage (usually not good to forgo it)

- Usually simple to qualify for all else equal

- Have the choice to prepay or refinance if and while you need

The Unhealthy

- There are closing prices related to a mortgage

- It may possibly take 30-45 days or longer to get one

- You must pay curiosity every month to the lender

- As a result of most loans final 30 years it quantities to a ton of curiosity

- Might carry mortgage into retirement, which is usually not suggested

- Requires you to hold sure stage of householders insurance coverage

Learn on: Do I actually own my home if I have a mortgage?

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) residence consumers higher navigate the house mortgage course of. Comply with me on Twitter for warm takes.