Firm overview

Hyundai Motor India Ltd. (HMIL) is part of the Hyundai Motor Group, the third largest auto authentic tools producer (OEM) on this planet based mostly on passenger autos gross sales in CY23. HMIL is the second largest auto OEM within the Indian passenger autos market since FY09 (by way of home gross sales quantity). The corporate has a portfolio of 13 fashions of passenger car segments by physique varieties similar to sedans, hatchbacks, sports-utility autos (SUVs) and battery electrical autos (EV). The corporate additionally manufactures elements, similar to transmissions and engines which might be used for its personal manufacturing or gross sales. Additionally it is the nation’s second largest exporter of passenger autos. From 1998 to 30 June 2024, the corporate has cumulatively bought greater than 12 million models of passenger autos in India and thru exports. The corporate’s manufacturing services are situated in Tamil Nadu, with a present manufacturing capability of 824,000 (as of 30 June 2024).

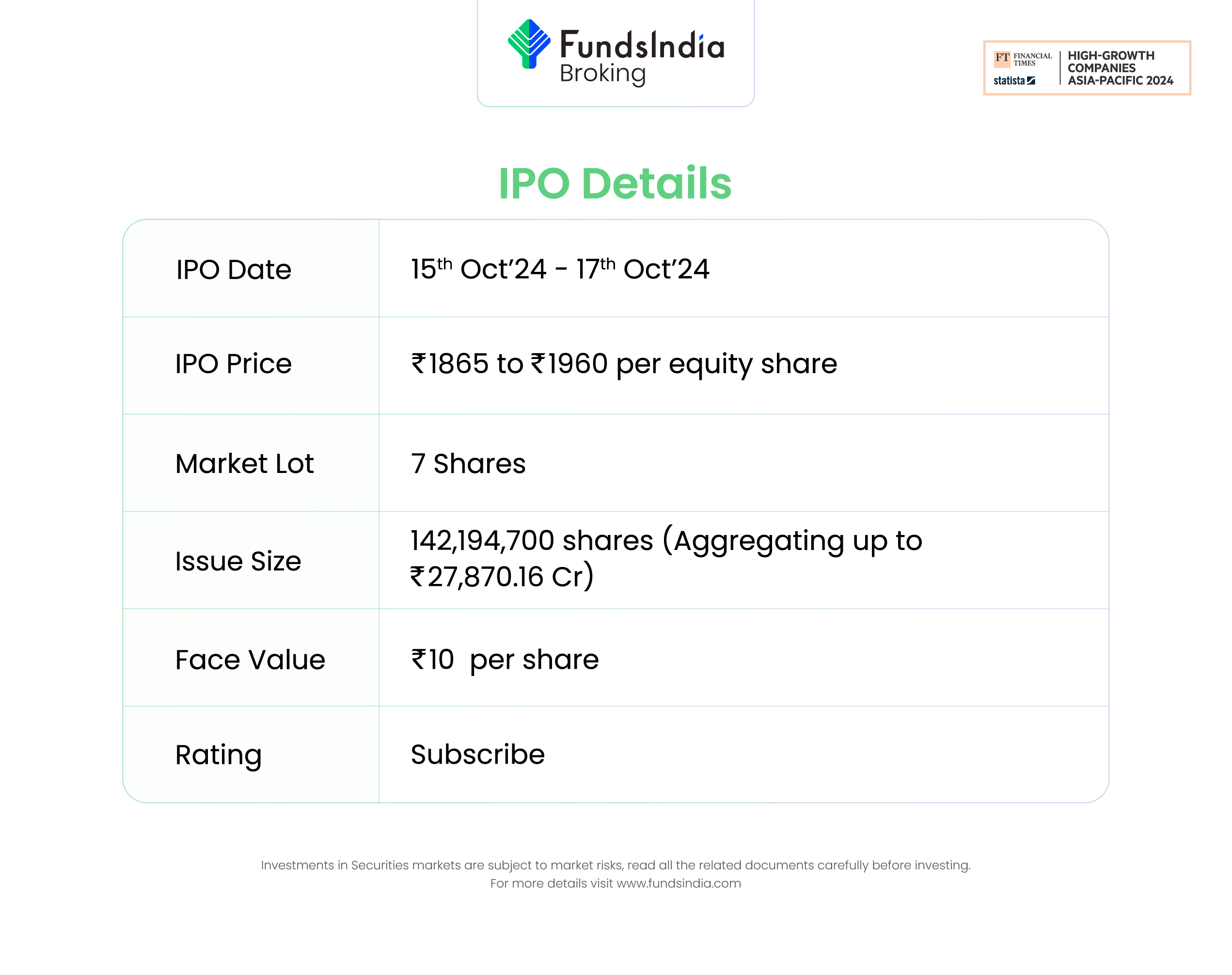

Objects of the provide

- Obtain the advantages of itemizing the Fairness Shares on the Inventory Exchanges.

- Perform provide on the market of as much as 142,194,700 Fairness Shares by the Promoting Shareholders.

Funding Rationale

- Sturdy parentage of Hyundai – The corporate positive aspects vital benefits from its sturdy affiliation with Hyundai Motor Firm (HMC). It advantages from varied operational features, together with administration, analysis and growth, design, product planning, manufacturing, provide chain growth, high quality management, advertising and distribution, model worth, and financing. Moreover, HMC’s intensive gross sales community, overlaying 190 international locations, enhances the corporate’s export alternatives, that are important for income. The corporate harness international insights and R&D capabilities to combine expertise, design, and aesthetics into passenger autos particularly tailor-made for the Indian market.

- Development methods – To handle the growing demand, the corporate is scaling its manufacturing capability. As of June 30, 2024, it operates two manufacturing services in Tamil Nadu, with an annual manufacturing capability of 824,000 models, working at practically full capability. Throughout FY24, the corporate acquired the Talegaon Manufacturing Plant from Basic Motors India, to be operational in phases, with the primary section anticipated to be operational in H2FY26. The Talegaon Manufacturing Plant is an built-in passenger car and engine manufacturing facility throughout roughly 300 acres of leased land allotted by the commercial growth company premises. The corporate expects the annual manufacturing capability throughout all of the manufacturing vegetation in combination to extend to 994,000 models when the Talegaon Manufacturing Plant is partly operational and to 1,074,000 models as soon as the Talegaon Manufacturing Plant is totally operational. With the addition of Talegaon plant, the corporate is aiming to spice up manufacturing quantity and speed up economies of scale to match its provide chain capabilities in step with the rising demand in home in addition to worldwide markets.

- Monetary Monitor Document – The corporate reported a income of Rs.69,820 crore in FY24 as in opposition to Rs.60,308 crore in FY23, a rise of 16% YoY. The income has grown at a CAGR of 21% between FY22-24. The EBITDA of the corporate in FY24 is at Rs.9,133 crore and EBITDA margin is at 13%. The PAT of the corporate in FY24 is at Rs.6,060 crore and PAT margin is at 9%. The CAGR between FY22-24 of EBITDA is 29% and PAT is 45%. The Return on Web Price and Return on Capital Employed of the corporate stands at 12.26% and 13.69% as of 30 June 2024, respectively.

Key dangers

- OFS danger – The IPO consists of solely an Supply for Sale of as much as 142,194,700 Fairness Shares by the Promoting Shareholders, Hyundai Motor Firm. Your complete proceeds from the Supply for Sale will probably be paid to the Promoting Shareholders and the Firm won’t obtain any such proceeds.

- Macroeconomic components – Any slowdown within the family earnings attributable to macroeconomic components may impression the demand and thereby the corporate turnover.

- Tech modifications – The lack of the corporate to adapt to the quickly evolving international automotive trade, resulting in modifications in expertise utilization, may adversely have an effect on the market share the corporate at present holds.

Outlook

The corporate advantages from the sturdy parentage of Hyundai Motors. The corporate has gained market place from (i) broad product choices, (ii) stakeholder relationships and operations; (iii) the sturdy Hyundai model in India; (iv) capacity to leverage new applied sciences to boost operational and manufacturing effectivity; and (v) capacity to increase into new companies similar to EVs by innovation. In keeping with RHP, Maruti Suzuki India Ltd, Tata Motors Ltd and Mahindra & Mahindra Ltd are the one listed competitor for Hyundai Motor India. The friends are buying and selling at a median P/E of 23.57x with the best P/E of 29.96x and the bottom being 11.36x. On the larger value band, the itemizing market cap of Hyundai Motor India will probably be round ~Rs.1,59,258 crore and the corporate is demanding a P/E a number of of 26.28x based mostly on submit difficulty diluted FY24 EPS of Rs.74.58. When put next with its friends, the problem appears to be totally priced in (pretty valued). Based mostly on the above views, we offer a ‘Subscribe’ ranking for this IPO for a medium to long-term Holding.

Different articles chances are you’ll like

Put up Views:

975