President-elect Trump is choosing his employees appointees who’re perceived by some to be controversial, unqualified, and even extremists. The justification is commonly that they’re disruptors who will problem the established order. The rhetoric is growing about including tariffs, eliminating businesses, lowering laws, and slicing Federal spending and employees. Rhetoric strikes markets. This text is about defending our portfolios from chaos throughout occasions of excessive uncertainty.

In the course of the first three years of President Trump’s first time period, Federal spending elevated by 9 % after adjusting for inflation. This was partly as a result of the 2017 tax cuts didn’t generate adequate progress to pay for themselves. In the course of the subsequent 4 years with the pandemic-era stimulus, Federal spending elevated by an extra seventeen % adjusted for inflation. Federal spending is now roughly $7.1 trillion with a deficit of $1.7 trillion that’s financed by including to the roughly $36 trillion in nationwide debt with curiosity prices of $1 trillion to finance that debt. This isn’t sustainable.

I count on sluggish progress this coming decade as a result of inhabitants progress continues to sluggish and is a key driver of financial progress, Federal spending is a part of the financial system, and slicing it should be offset by different drivers. Tariffs are inflationary, and rates of interest should keep increased for longer to finance the nationwide debt. With inventory evaluations and rates of interest excessive, returns over the intermediate time period favor bonds. One other issue to think about is that the greenback has superior practically 40% since 2011 which has stored import prices low, but additionally seems overvalued.

To guage a Chaos Protected Portfolio, I chosen between 1,600 to three,300 funds from every of the 2000, 2010, and 2020 a long time and ranked them primarily based on threat and return metrics. The highest-ranked funds have been mixed and ranked by risk-adjusted efficiency for the Dotcom, Nice Monetary Disaster, and COVID full cycles in addition to the previous twenty-five years.

There are some free similarities between now and the Dotcom Full Cycle from September 2000 to October 2007 as proven beneath. The top outcome was that the S&P 500 fell 45% through the Dotcom bear market.

- The S&P 500 price-to-earnings ratio hovered between 27 and 46 throughout 2000 and 2001 in comparison with practically 31 now.

- The greenback fell 25% from 2002 to 2008.

- Inflation hovered between 2.0% and three.5%.

- The Federal Funds fee went from 6.5% in mid-2000 to 1% in 2004 and again as much as 5.3% in 2007.

- Actual Gross Home Product went from 4% in 2000 to 1% in 2001 to three.8% in 2004 and again right down to 2% in 2007. A gentle recession occurred.

- Gold went from $293 per ounce in 2000 to $696 in 2007. It’s now $2,685.

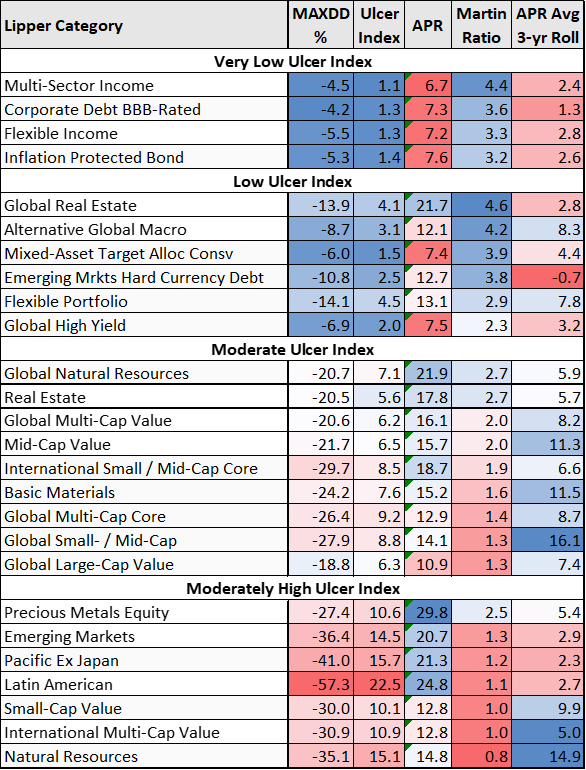

Desk #1 reveals among the best-performing Lipper Classes through the Dotcom full cycle from September 2000 to October 2007. For comparability functions, over the total cycle, the Ulcer Index of the S&P 500 was 22, the annualized % return was 1.9%, and the Martin Ratio was -0.1. The Ulcer Index measures threat because the depth and size of drawdowns, and the Martin Ratio is a measure of risk-adjusted returns.

Desk #1: Lipper Classes for the Chaos Protected Portfolio (Full Cycle September 2000 to October 2007)

Supply: Writer Utilizing MFO Premium fund screener and Lipper international dataset.

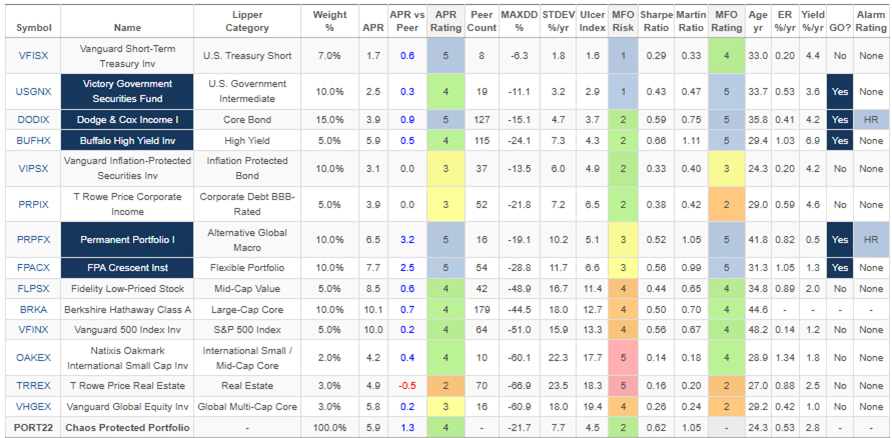

I created an all-weather portfolio for the previous twenty-five years as proven in Desk #2. There’s a tradeoff between threat and return. A youthful me aggressively invested 100% in shares, whereas an older and extra conservative me now holds a conventional 60% inventory to 40% bond allocation primarily based on matching withdrawal wants with time horizons utilizing the Bucket Strategy. The Chaos Protected Portfolio displays my private biases that one ought to keep diversified portfolios, and within the coming decade, I count on bonds to carry out higher than shares on a risk-adjusted foundation. The Chaos Protected Portfolio would have returned 5.9% with a most drawdown of twenty-two% over the previous twenty-five years in comparison with a return of 10% for the S&P 500 with a most drawdown of 51%. MFO Threat for the Chaos Protected Portfolio is estimated to be “2” for Conservative, and the APR ranking is Above Common.

Desk #2: Chaos Protected Portfolio (25.8 Years)

Supply: Writer Utilizing MFO Premium fund screener and Lipper international dataset.

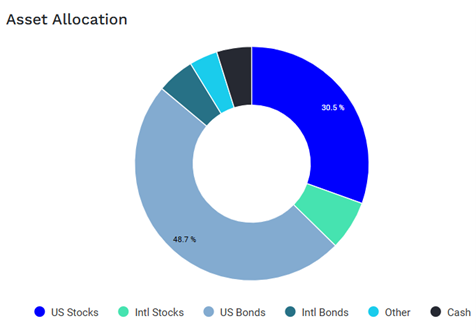

I used Portfolio Visualizer to see the present asset allocation of the portfolio which is about 37% shares with seven % allotted to worldwide shares.

Determine #1: Chaos Protected Portfolio Asset Allocation

Supply: Writer Utilizing Portfolio Visualizer – Backtest Portfolio Asset Allocation

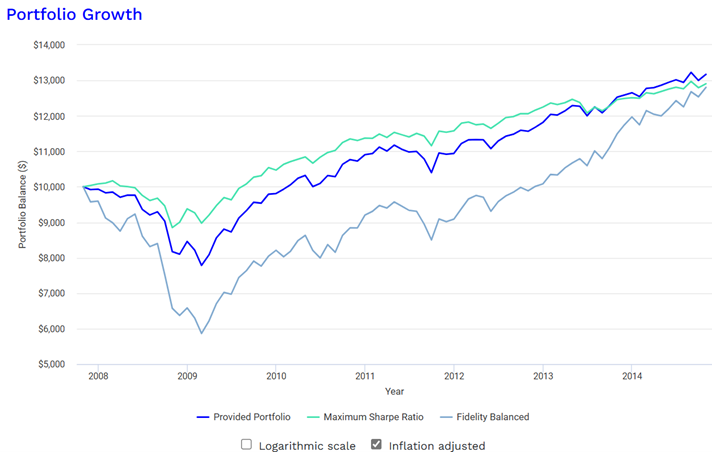

Determine #2 reveals how the Chaos Protected Portfolio would have carried out through the Nice Monetary Disaster in comparison with the identical funds that maximized the Sharpe Ratio and to the Constancy Balanced fund. The returns are adjusted for inflation. It could have taken seven years for the Constancy Balanced Portfolio to catch as much as the extent of the Chaos Protected Portfolio. This is called “sequence of return threat”.

Determine #2: Chaos Protected Portfolio Efficiency In the course of the Nice Monetary Disaster

Supply: Writer Utilizing Portfolio Visualizer – Portfolio Optimization – Great Financial Crisis

I’m at the moment studying How to Retire: 20 Lessons for a Happy, Successful, and Wealthy Retirement by Christine Benz, Director of Private Finance and Retirement Planning for Morningstar which was launched in September. There’s a wealth of data in it even for these of us already in retirement. She factors out that sources of withdrawals needs to be primarily based on market situations, and blended asset funds is probably not as advantageous as a combination of inventory and bond funds for choosing the place to withdraw funds. She advocates allocating ten % to money as a result of in some years each shares and bonds could carry out poorly. One other level that I discover helpful is to construction your portfolio to be versatile with withdrawals and match discretionary spending to market situations.

Extending tax cuts are prone to have a optimistic impact on shares in 2025 and maybe 2026 however with excessive valuations, returns will most likely be dampened. Excessive normal deductions and decrease tax charges will assist retirees. There can be winners and losers in tariff wars. Deregulation will assist monetary establishments, however enhance threat.

I exploit Constancy to handle a portion of my belongings utilizing the enterprise cycle method, and Vanguard to handle a portion utilizing a low-cost buy-and-hold method. I handle the remaining primarily based on my expectations. I’ve adjusted a part of my portfolio together with the ideas on this Chaos Protected Portfolio article and the Bucket Strategy advocated by Ms. Benz. By small changes and rebalancing, my allocation to shares has been decreased by about three proportion factors. I view this as taking a bit threat off the desk after the latest rise within the inventory market. I focus threat in my Bucket #3 for long-term progress and to reduce taxes.

I keep diversified bond funds in my conservative tax-advantaged accounts. With rates of interest excessive and a gentle touchdown doubtless, I not too long ago elevated allocations to reasonably riskier actively managed bond funds together with Vanguard World Credit score Bond (VGCIX), Vanguard Intermediate-Time period Funding-Grade (VFICX), Vanguard Multi-Sector Earnings Bond (VMSIX), and Fidelity Advisor Strategic Income (FADMX/FSIAX). That is in line with this text of constructing a Chaos Protected Portfolio. I want these funds to Excessive Yield funds.

I’ve appointments arrange with my advisors subsequent yr to withdraw from extra aggressive tax-advantaged accounts as a substitute of conservative accounts to additional pull a bit threat off the desk whereas replenishing Bucket #1 for residing bills.

Take pleasure in a secure and completely satisfied vacation season!